Top_Vola incorporates a dynamic volatility overlay designed to benefit from volatility and risk premia over time, while adapting exposure as market stress conditions change.

- Equity exposure is complemented by volatility-linked components

- Positioning adapts as volatility rises or declines

- All adjustments follow predefined, rule-based signals

Top_Research represents the complete universe of rule-based trading strategies, which are systematically implemented within the GR_Strategies portfolios in both USD and EUR.

| Date | Top_Vola | DAX | SP500 |

|---|---|---|---|

| 0.06 % | -0.16 % | ||

| -0.60 % | -0.63 % | ||

| 1.45 % | 9.40 % | ||

| 78.45 % | 102.94 % | ||

| 17.27 % | 21.49 % | ||

| 1.15 | 1.44 |

Risk-aware allocation framework

The strategy

continuously evaluates the relative risk characteristics of equity

markets and volatility instruments. Based on this assessment, portfolio

weights are dynamically adjusted to balance participation in equity

returns with exposure to volatility as a risk-management tool. All

adjustments follow predefined, systematic rules and are implemented with

appropriate safeguards to ensure robustness.

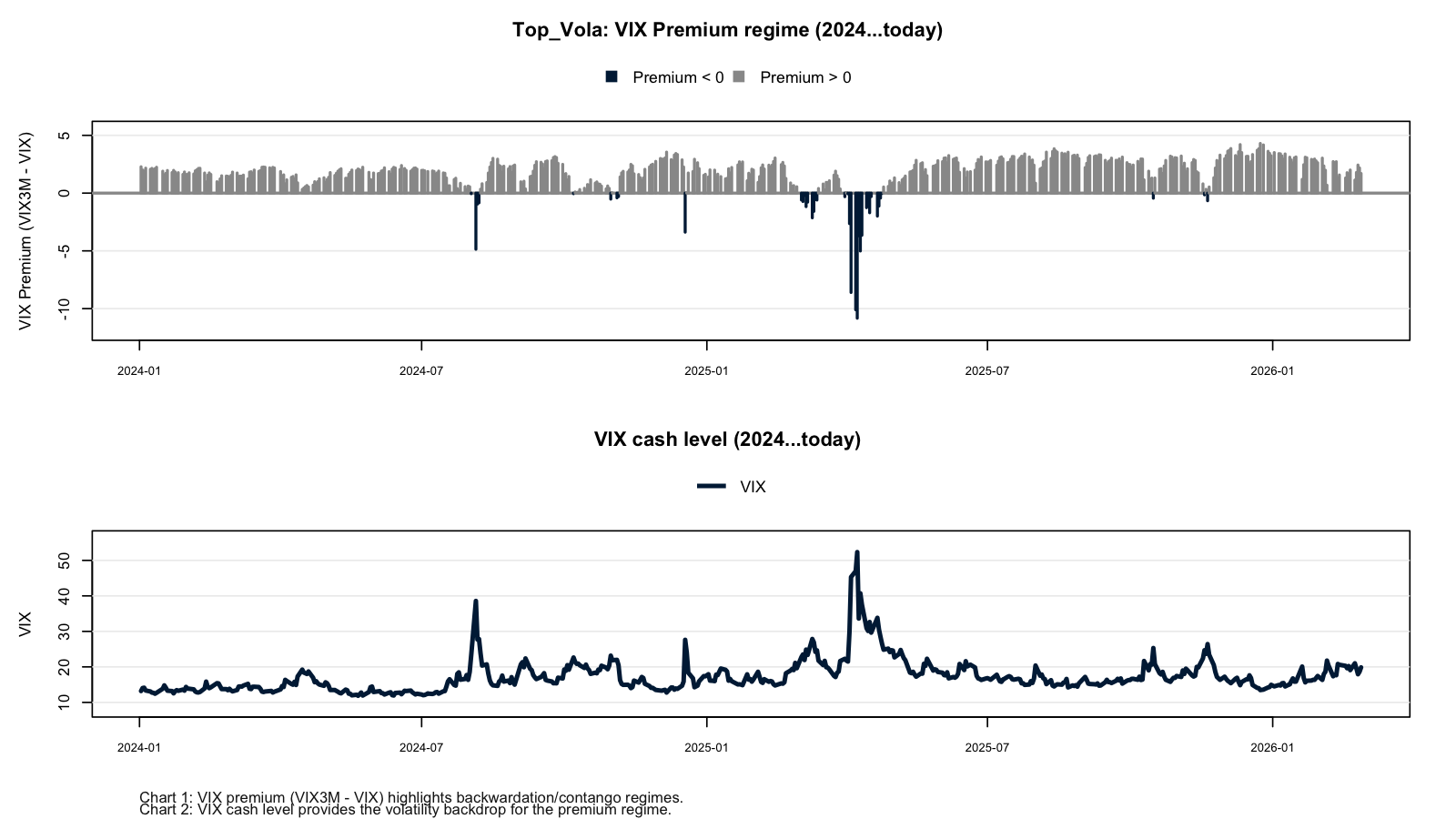

Volatility regime assessment

In addition to

relative risk measures, the strategy incorporates information from the

volatility term structure to distinguish between normal market

conditions and periods of elevated stress. This regime assessment

determines whether volatility exposure is used as a stabilizing overlay

or as a protective component.

Portfolio construction

Equity and volatility

contributions are combined using dynamically adjusted weights. Depending

on the volatility regime, the strategy may benefit from volatility carry

in calmer environments or seek convex protection during stressed market

phases. The overall construction is designed to respond adaptively

without relying on market forecasts or discretionary decisions.

Objective

Top_Vola aims to participate in equity

upside while actively managing volatility exposure as an integral part

of the strategy. By combining systematic risk assessment with a

regime-aware volatility overlay, the strategy seeks to deliver a more

resilient return profile across diverse market environments.

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | Year | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2023 | |||||||||||||

| 2024 | |||||||||||||

| 2025 | |||||||||||||

| 2026 |

Performance Metrics

| Top_Vola | |

|---|---|

| Cumulative Return (%) | 140.91 |

| Ann. Return (%) | 28.34 |

| Ann. Sharpe Ratio | 1.44 |

| MAR Ratio | 1.74 |

Risk Metrics

| Top_Vola | |

|---|---|

| Ann. StdDev. (%) | 19.64 |

| SemiDeviation (%) | 0.93 |

| Max DrawDown (%) | 16.28 |

| Value-at-Risk (%) | -2.04 |

Daily Metrics

| daily metrics (%) | |

|---|---|

| Av. Return (%) | 0.11 |

| Best Day (%) | 5.89 |

| Worst Day (%) | -6.01 |

| Av. Up-Day (%) | 0.86 |

| Av. Down-Day (%) | -0.99 |

| Pct Up-Days (%) | 59.00 |

| Pct Down-Days (%) | 41.00 |

Monthly Metrics

| monthly metrics (%) | |

|---|---|

| Av. Return (%) | 1.98 |

| Best Month (%) | 13.29 |

| Worst Month (%) | -11.20 |

| Av. Up-Month (%) | 4.90 |

| Av. Down-Month (%) | -3.27 |

| Pct Up-Months (%) | 64.00 |

| Pct Down-Months (%) | 36.00 |

| From | Trough | To / Recovery | Depth | Days |

|---|---|---|---|---|

| 2026-01-13 | 2026-03-30 | 2026-05-29 | -16.28 % | 95 |

| 2024-07-17 | 2024-08-02 | 2024-12-24 | -12.93 % | 113 |

| 2023-09-15 | 2023-10-27 | 2023-11-20 | -12.80 % | 47 |

| 2023-02-03 | 2023-03-13 | 2023-04-18 | -10.53 % | 51 |

| 2025-10-09 | 2025-11-21 | 2026-01-06 | -10.13 % | 61 |

| Top_Vola | TLT | VNQ | UUP | EFA | DBC | GLD | DAX | SPY | |

|---|---|---|---|---|---|---|---|---|---|

| Annualized Return | 27.4% | -0.9% | 9.4% | 4.5% | 16.6% | 8.6% | 23.7% | 17.3% | 21.5% |

| Annualized Std Dev | 19.3% | 14.1% | 17.1% | 6.7% | 14.8% | 16.3% | 19.5% | 15.0% | 14.9% |

| Annualized Sharpe | 1.42 | -0.06 | 0.55 | 0.67 | 1.12 | 0.53 | 1.21 | 1.15 | 1.44 |

| Worst Drawdown | 16.3% | 22.4% | 21.8% | 10.1% | 14.1% | 16.5% | 26.4% | 16.0% | 18.8% |

More analysis for Top_Vola

| Top_Vola | TLT | VNQ | UUP | EFA | DBC | GLD | SPY | DAX | |

|---|---|---|---|---|---|---|---|---|---|

| Annualized Return | 21.3% | 1.2% | 7.5% | 3.6% | 6.4% | 2.3% | 9.4% | 13.3% | 7.6% |

| Annualized Std Dev | 20.8% | 14.3% | 19.4% | 7.0% | 16.7% | 17.3% | 15.8% | 17.0% | 18.7% |

| Annualized Sharpe | 1.02 | 0.08 | 0.38 | 0.52 | 0.38 | 0.13 | 0.59 | 0.78 | 0.41 |

| Worst Drawdown | 29.2% | 48.4% | 42.4% | 14.2% | 34.2% | 59.9% | 26.4% | 33.7% | 38.8% |

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | Year | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2014 | |||||||||||||

| 2015 | |||||||||||||

| 2016 | |||||||||||||

| 2017 | |||||||||||||

| 2018 | |||||||||||||

| 2019 | |||||||||||||

| 2020 | |||||||||||||

| 2021 | |||||||||||||

| 2022 | |||||||||||||

| 2023 | |||||||||||||

| 2024 | |||||||||||||

| 2025 | |||||||||||||

| 2026 |

My portfolio comprises:

- Top_Dual & Top_Target momentum and accumulation strategies, are focusing on harnessing and leveraging market trends for consistent and sustainable growth.

- Top_Switch, an Asset rotation strategy is dynamically reallocating capital across asset classes to optimize returns and mitigate risks.

- Top_Vola strategy, is tailored to capitalize on both sudden and sustained market fluctuations, enhancing risk - adjusted returns.

- Top_Rank, a systematic ranking strategy that continuously allocates capital to the strongest-performing assets, ensuring disciplined participation in prevailing market leadership.

- Top_Trend (=CTA) strategy, which forms the backbone of diversification with a 30 % allocation. This strategy excels in capturing trends and providing stability during market

- Additional advanced and highly specialized approaches, crafted to adapt seamlessly to complex and evolving market dynamics.

Together, these strategies create a robust and well - balanced portfolio framework. By blending simplicity with sophistication, the approach ensures adaptability, consistency, and long - term success, even in the face of unpredictable market conditions.

Uncorrelated Strategies

The cornerstone of success lies in the deliberate and precise integration of diverse, genuinely uncorrelated strategies, executed with unwavering discipline and emotional composure. My approach is devoid of the influence of greed or fear, guided instead by the principles of expertise and professionalism. Each decision is the product of meticulous analysis and a technically sound methodology, consciously avoiding impulsive or reactionary behavior. Furthermore, all decisions are grounded 100% in mathematical and statistical principles, ensuring objectivity and consistency. By consciously excluding any human influence, the process eliminates the risk of emotional bias or subjective judgment. This steadfast adherence to strategy allows me to navigate the complexities of the markets with confidence and consistency, maintaining an unyielding commitment to excellence.

Trading

The elegance of these strategies lies in their straightforward yet effective design. Each morning, data is carefully downloaded, and within 15 minutes, calculations ensure that theoretical models align seamlessly with practical execution. By evening, new orders are automatically dispatched to the exchange, just before the market closes. This approach is not a feat of magic, but rather a testament to disciplined craftsmanship. It guarantees that execution timing remains uninfluenced — an essential factor in maintaining the robustness and reliability of the strategy.

Data Used

Back-testing is often dismissed as mere theory or abstract mathematics. However, I recognize that the performance up to December 2022 reflects a combination of real - time trading outcomes and newly implemented systems. While historical achievements provide valuable insights, I find little satisfaction in endlessly revisiting past successes. My focus is clear and uncompromising—cutting through bureaucracy to channel my energy toward the present and future, where true progress is made.

Dedication

In collaboration with my dear friend and developer, Helmuth Vollmeier, in a fit of genius or maybe just sheer madness, we decided to hit the reset button on everything in 2022. It was like a software update for our lives — new and improved. Unfortunately, the joy of our new start was short-lived as Helmuth passed away suddenly in February 2023, leaving me deeply saddened. Despite facing phases of doubt and questioning the meaning of it all, I returned to my desk, immersing myself in learning once again, now without my dear friend Helmuth by my side! I dedicate this work to Helmuth Vollmeier, one of my best friends, my intellectual partner, my daily communicator, and companion!

Top Dual Top Switch Top Target Top Rank ✓ Top Vola Top Trend